On January 7th local time, US President Trump announced on social media that he would push for legislation to prohibit large institutional investors from purchasing single-family homes, in an effort to alleviate the housing pressure on ordinary families. This policy targets institutional investors such as Blackstone Group (BX), whose business model of purchasing, holding and renting out single-family homes through cash acquisitions is facing a direct impact. The market reacted promptly:

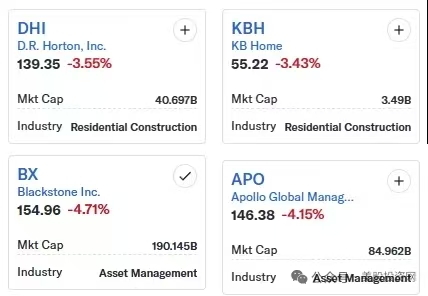

The share price of Blackstone Group plummeted as the market was concerned that its long-term asset expansion strategy had been "cut off" by policies.

House builders (such as TOL and KBH) have experienced a simultaneous decline, and the uncertainty regarding short-term demand has triggered panic.

The fluctuations in the real estate sector have intensified, reflecting the market's profound anxiety over the cascading effects of policies.

Although the policy is aimed at lowering the purchase threshold for ordinary families, the short-term market still faces some difficulties:

Decline in institutional buying: Institutional investors were originally the "stabilizing absorbers" of the new housing market. Their withdrawal may lead to a slowdown in the rate of new housing inventory clearance in the short term.

2. Expectation for housing price increase has been dampened: Developers' valuation is based on the steady rise of housing prices. After the policy clearly sets the goal of "reducing housing prices", the market may reevaluate its gross profit margin and growth logic.

3. Emotion-driven trading: The increase in uncertainty prompts investors to seek safety, but the impact is mainly driven by the emotional aspect rather than a fundamental collapse.

From a structural perspective, this move may drive the US real estate sector towards a more sustainable development path:

1. Housing affordability improves: The fierce competition among institutions weakens, housing price growth slows down, and the entry threshold for first-time buyers is lowered;

2. Shift in transaction focus: The market has shifted from being "driven by capital" to "driven by residential demand", and the proportion of owner-occupiers relying on mortgage loans has increased;

3. Optimize business model: The profit model of real estate developers shifts from relying on price increases to improving turnover rates. Healthy transaction volume becomes the core indicator.

Under the policy reshaping, two types of assets are expected to stand out:

Mortgage service provider (such as Rocket Companies, RKT):

· The number of institutional cash buyers has decreased, while the penetration rate of mortgage loans has structurally increased;

The release of the demand for self-occupied housing directly drove the increase in loan issuance and refinancing business.

The potential for uncovering long-term customer value (such as insurance and net loan services) has expanded.

2. Project-oriented builders:

The product is positioned at the mid-to-low end and focuses on affordability, aiming to meet the demand growth.

If the policies are accompanied by land supply and tax incentives, the leading construction companies still have the potential for consolidation.

Over the past few years, institutions such as private equity funds, hedge funds and REITs have, with their advantages of full cash payment and aggressive bidding, carried out large-scale acquisitions of single-family homes, significantly intensifying the competitive pressure on ordinary home buyers. Once policy restrictions are implemented, it will lead to:

· The tide of aggressive cash buying is receding: One of the most powerful purchasing forces in the market will significantly weaken.

· Housing prices expected to stabilize: The rapid growth of housing prices has lost its main driving force, which is conducive to stabilizing market expectations.

· The entry barrier for owner-occupiers has been lowered: For ordinary families, especially first-time buyers, their relative disadvantage in the bidding process will be reduced, and the feasibility of purchasing a home will increase.

Business Association Interpretation: Essentially, this involves moving a portion of the housing inventory from the "capital investment goods" category back to the "housing consumer goods" category, thereby directly expanding the base of potential customers for RKT.

The core of RKT's profitability is directly linked to transaction volume and loan issuance scale, rather than changes in house prices. The improvement in market affordability will trigger the following positive cycle:

The pool of potential buyers has expanded: more families have entered the "affordable" range.

2. Transaction activities recover: Increased confidence in purchasing decisions has led to a rise in the number of house transactions.

3. Growth in core business volume: The scale of loan applications and disbursements has increased accordingly, directly driving the most significant revenue growth for RKT.

From the perspective of the chamber of commerce: For platforms like RKT, the "activity level" of the market is more crucial than the "price level". The policy of lowering the threshold to activate transactions precisely hits the core of their business model.

The policy will fundamentally change the payment structure of market transactions:

Previously: The institution-led all-cash transaction did not involve any mortgage lending business and had no direct value for RKT.

· Since then: The market has been dominated by owner-occupiers who rely on mortgages, and mortgage loans have become the core financial component of the vast majority of transactions.

This transformation implies that the mortgage penetration rate across the entire market will undergo a structural increase, providing a broader and more stable market share foundation for RKT's loan issuance business.

The increase in owner-occupier buyers has brought RKT not only one-time loan profits, but also the starting point for long-term customer relationships:

· Subsequent financial needs: The client may have ongoing requirements such as refinancing or home equity line of credit (HELOC).

· Deepening of customer value: A stable and long-term customer base makes it easier to uncover higher customer lifetime value.

· Cross-selling opportunities: Based on the housing finance relationship, it is possible to effectively extend to other products such as insurance and auto finance.

In summary, this policy achieves the following through the transmission path of "suppressing irrational competition → enhancing affordability → activating self-ownership transactions → optimizing payment structure":

Reduce the impact of cash buyers → Improve housing affordability → Significantly increase the number of home buyers relying on mortgage loans

This represents a clear and sustainable fundamental positive for institutions whose core driving force is transaction volume and loan scale. Investors should pay attention to the changes in trading activity and the volume of RKT loan issuances in key markets (especially the mid-to-low-priced housing market) after the policy is implemented, in order to verify the realization of this logic.

China-US Real Estate Chamber of Commerce

Note: The China-US Real Estate Chamber of Commerce will continue to monitor the progress of policy implementation and provide customized insights and resource connection services for its members.

(This article is based on publicly available information and does not constitute investment advice. The market carries risks. Independent decision-making is necessary.)

Email: info@sinoamericanrec.org

Tel: +1(626)-658-6066

Office Address(Expect):Los Angeles county

Follow to our WeChat or leave a message in the form.

SAREC is a high-end cross-border platform that connects real estate developers, investment elites, fund managers, financial institutions and professional service providers in China and the United States.

Email: info@sinoamericanrec.org

Tel: +1(626)-658-6066

Office Address:Los Angeles county

If you have a project or collaboration that you would like to discuss with us, or if you would like to know what solutions we can provide for you, we look forward to your consultation.

Contact Tel

Follow to our WeChat or leave a message in the form.

English

English